💡

This report was offered by a group member. Whereas Synthetix has reviewed the content material for veracity, these views will not be essentially endorsed by the Synthetix DAO and/or group.

Lyra protocol gives decentralized choices infrastructure using Synthethix infrastructure to assist margining and hedging for LPs. Choices are sometimes troublesome for the common consumer to wrap their head round in comparison with perpetual futures, so on this article we’ll cowl all you could find out about choices + how Lyra gives infrastructure to commerce them.

Choices Primer

There’s one million completely different guides to choices on the market proper now – for those who’ve by no means heard of them earlier than there’s fairly a deep rabbit gap to go down. On the danger of sounding like a damaged report, I’ll restate a few of that primer materials right here to assist set the scene for Lyra. You’ll be able to skip this part for those who’re already accustomed to what choices contracts are.

An choice contract is an settlement between a purchaser and a vendor to purchase or promote a selected asset on a specified expiration date sooner or later (expiry date) at a selected worth (strike worth). We now have name choices and put choices – Name choices symbolize the contract purchaser’s proper to buy the asset sooner or later, whereas put choices symbolize the contract purchaser’s proper to promote the asset sooner or later.

The vendor of the contract is then obligated to promote the consumer that asset (or buy it from then, for put contracts) ought to the contract expire “in-the-money.” The vendor collects a premium from the customer when the commerce is opened (this premium is commonly priced by a sophisticated pricing mannequin, extra on that later) – and if the contract expires “out-of-the-money,” the vendor will get to maintain the premium and has no obligation to settle the contract. Let’s check out two fast examples.

So, with these two fundamental contracts we have now 4 completely different trades. Shopping for a name (bullish), promoting a name (bearish), Shopping for a put (bearish), and promoting a put (bullish). With these 4 we are able to create a complete host of sophisticated methods. Right here yow will discover some extra advanced methods, tips on how to execute them, and what sort of biases they match.

When placing contracts like this onchain, we’re confronted with a few key hurdles. One in every of them being pricing. Present choices pricing fashions in tradfi aren’t precisely excellent for tokens – they’re made to cost choices in opposition to equities. One of many key variables they have a look at is implied volatility, which is the market’s opinion of the underlying asset’s probability to vary in worth. Tokens are clearly orders of magnitude extra unstable than equities, so if we use a standard choices pricing mannequin we’ll find yourself with mispriced premiums and low curiosity from consumers/sellers

The second hurdle is a well-recognized one all through all of defi – liquidity. The well-known chicken-and-egg drawback of needing to draw liquidity whereas concurrently attracting demand for that liquidity is a comparatively unified one for any defi protocol with a liquidity provisioning part. With choices particularly – not having sufficient liquidity can imply much less strike costs/expiries and decrease open curiosity (OI, the sum whole of all open trades in a given market) caps for merchants.

Lyra

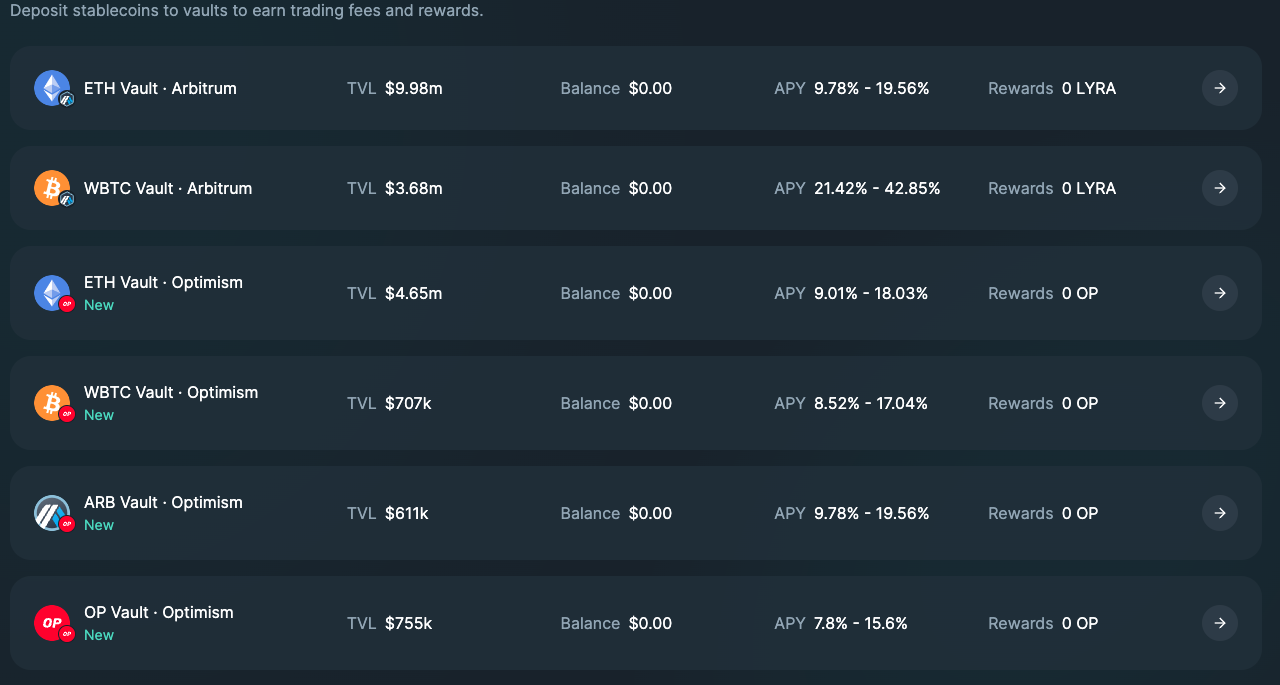

Lyra affords choices buying and selling in opposition to $ETH and $WBTC on Arbitrum and in opposition to $ETH, $WBTC, $ARB, and $OP on Optimism. Lyra choices are European-style, that means they’ll solely be exercised on the expiration date (versus American-style, which may be exercised on or earlier than the expiration date). Lyra segments liquidity suppliers from choices consumers/sellers, permitting any arbitrary commerce to be stuffed even with no direct counterparty, so long as the asset + strike worth is supported.

Offering Liquidity on Lyra

Lyra employs a peer-to-protocol method the place LPs deposit stablecoins into market maker vaults (MMVs) for particular belongings to gather buying and selling charges and hedged dealer PnL by serving as a counterparty for all merchants. To be able to defend LPs from a very one-sided buying and selling surroundings, Lyra additionally hedges for LPs through GMX (for merchants on Arbitrum) or Synthetix (for merchants on Optimism). On Optimism, for instance, LPs would deposit $USDC (this will get swapped to $sUSD if wanted to hedge) or $sUSD in an MMV. If Lyra merchants have a heavy lengthy bias unprotected MMV vaults could be pressured to have a heavy brief bias to fill these trades.

To be able to deposit/withdraw liquidity on Lyra, LPs must first sign the intention to take action – a three-day cooldown is then initiated the place the funds are locked after which deposited after the cooldown interval. The protocol has circuit breakers in place to keep up payouts for LPs + liquidity for merchants in case of insolvency. On this situation, withdrawals/deposits could also be blocked (though, further deposits may be manually authorized ought to they be blocked for lengthy sufficient).

Synthetix’s Position

Synthetix performs an important position for Lyra on Optimism. Lyra makes use of Synthetix Perps to hedge their choices AMM utilizing perps positions on Synthetix with a view to keep a delta-neutral place in MMVs, thus defending their LPs from pointless directional danger ought to choices merchants have a heavy lengthy or brief bias.

Tangentially, Kwenta additionally affords a frontend for buying and selling choices utilizing Lyra – making it a one-stop store for buying and selling Synthetix perps and Synthetix-margined choices.

APYs for LPs can vary between 8% – 40%, relying on market situations and which market you select to offer liquidity for.

Pricing

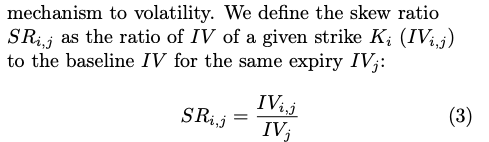

Precisely pricing choices is an important part of a profitable choices protocol. Worth too low, and choices sellers received’t have an interest. Worth too excessive, and choices consumers received’t have an interest. Choices pricing is historically executed utilizing the Black-Scholes mannequin, an equation that takes in 5 inputs – the one one which requires any tweaking to make the mannequin match for onchain choices is implied volatility, or IV (the opposite inputs are asset worth, strike worth, time-to-expiry, and the chance free price. Every of those may be utilized as they might in another choices alternate). IV is a quantity that represents the market’s opinion of an underlying asset’s probability to vary in worth and is completely different throughout every strike worth + expiry primarily based on provide/demand. Lyra IV calculation facilities round rising IV when demand for an choice with a selected strike + expiry is excessive and reducing IV when provide is excessive.

The above sentence is a fairly large oversimplification, so let’s dig a bit deeper. Lyra initializes a baseline IV for the ATM (the place strike worth = spot worth) choice at a given expiry utilizing present market information. This may be extrapolated to different strikes throughout the identical expiry by rising/reducing baseline IV per every trades inside that expiry (relative to whole variety of trades). This new baseline IV is then divided by the unique to find out skew ratio – which in flip tells us that skew ratio instances unique IV may give us an equation for figuring out IV for any strike with the identical expiry.

There’s one different bit about pricing price mentioning – Lyra’s administration of Vega danger. Vega is a measure of a contract’s sensitivity in worth to adjustments within the IV. Since there’s a restricted quantity of liquidity within the MMVs at any given time – there’s a certain quantity of Vega the system can safely tackle with out placing LPs vulnerable to insolvency ought to IV transfer an excessive amount of. To stop this – Lyra prices a payment (or affords a reduction) to assist the system keep net-zero Vega for MMVs.

So in summation – IV is the most important unknown consider figuring out an choices worth (you possibly can consider buying and selling an choice as buying and selling IV). Lyra protocol determines IV by initializing a baseline worth for the ATM strike, then has that dynamically change primarily based on demand + extrapolates it to different strikes throughout the identical expiry (+ repeats the method for different expiries). As well as – there’s a flat payment/low cost on high of the choices worth to keep up the system having impartial publicity to Vega (i.e, much less uncovered to huge volatility swings).

Buying and selling

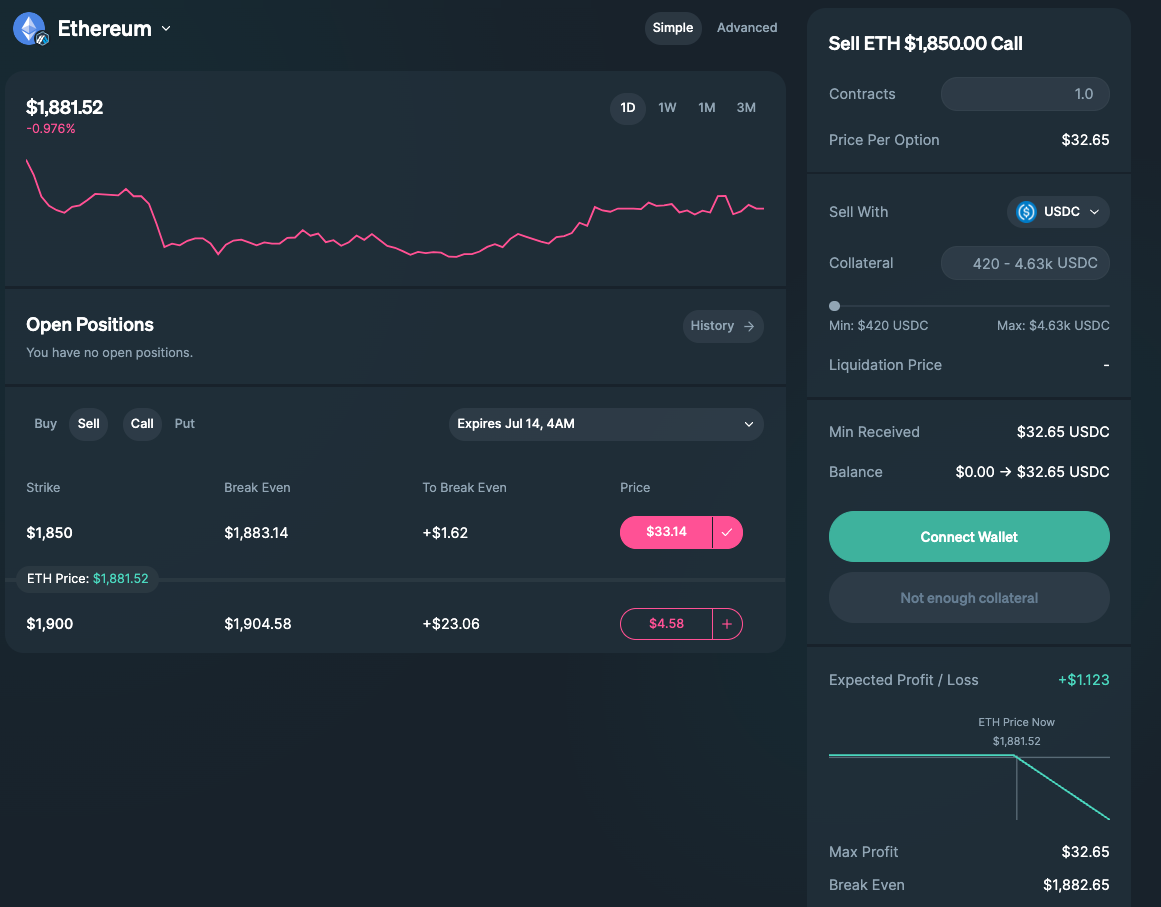

Lyra and Kwenta each supply (related) interfaces for buying and selling choices utilizing the Lyra Protocol. At the moment, they provide expiries as much as about 2 months upfront, with wherever from 1-10+ strikes per expiry. The buying and selling rewards program was additionally overhauled in April 2023 – at present, merchants earn rewards in proportion to their charges in $OP and $LYRA (they have been additionally paying out $ARB to Arbritrum merchants up till not too long ago – now paying $LYRA). They’ll additionally earn higher rewards by buying and selling shorted dated contracts and/or holding contracts till expiry. These rewards may be boosted by as much as 2.5x by having a better dealer rating (resets every day), staking $LYRA, or referrals (as much as 1.2x, referrals additionally supply buying and selling payment reductions like most derivatives platforms).

Lyra’s interface

Should you bear in mind from our two examples above – promoting (both a name or a put) would require exercising the consumers contract at expiry. Which means promoting choices requires some degree of collateralization to make sure correct settlement. The latest Newport improve allowed for partial collateralization of promoting choices on Lyra – executed so in both or the quote ($USDC/$sUSD) or the bottom asset ($ETH/$BTC/and so on.). There are a few notable limitations to buying and selling, particularly:

Merchants can not open positions for choices expiring in below 12 hoursTraders can not open trades which have deltas (delta is a measure of how a lot the worth of an choices contract will transfer given a $1 transfer within the underlying asset) outdoors a specified cutoff rangeFor closing trades which can be outdoors these two parameters – they need to accomplish that utilizing the ForceClose mechanism, incurring a penalty

Bear in mind additionally that charges dynamically replicate the online whole IV within the AMM – so they’re additionally topic to further charges ought to trades exacerbate the Vega.

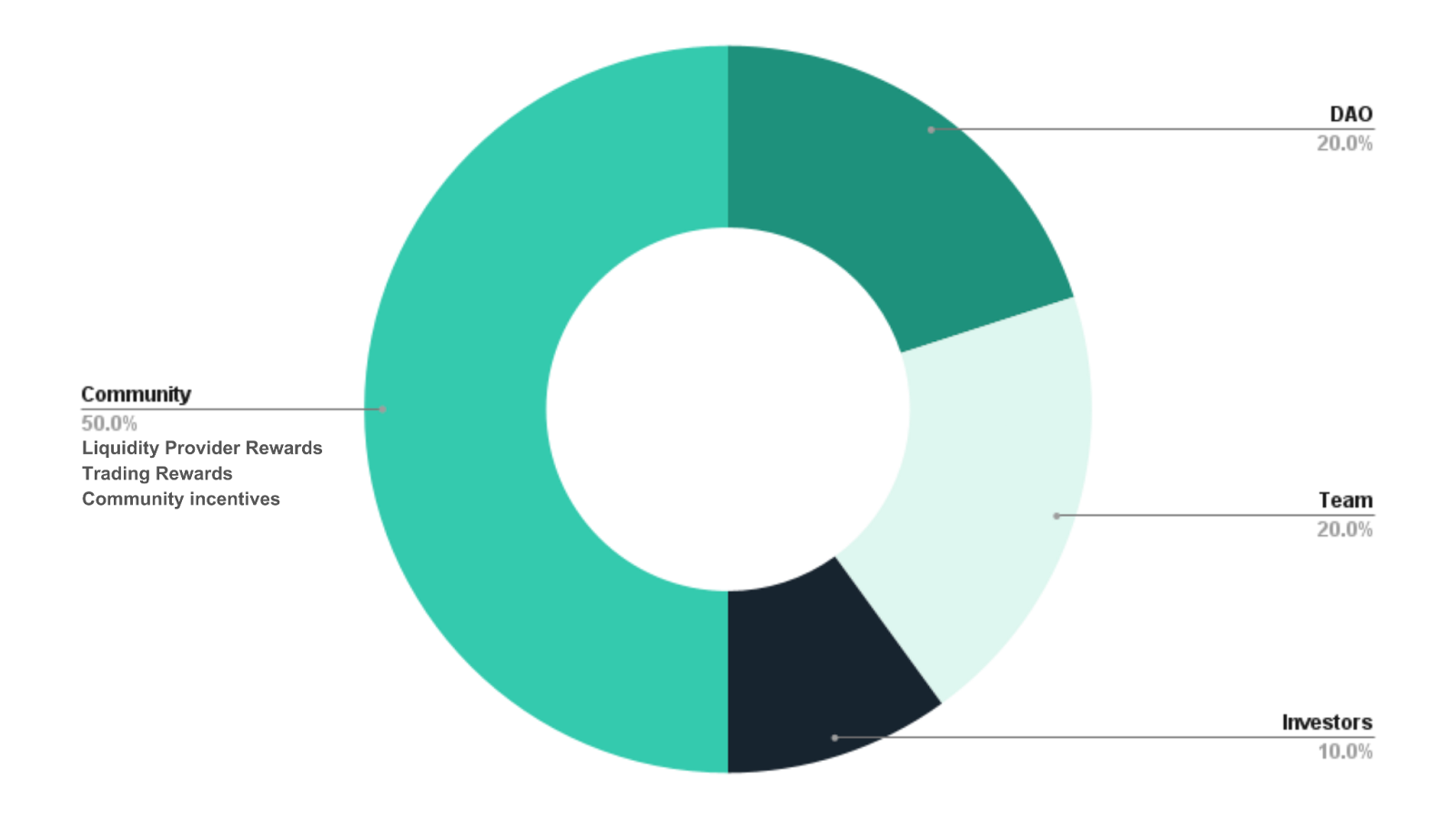

Tokenomics

$LYRA is the governing token of Lyra protocol. Staking permits for participation in governance (or delegation of governance) in addition to boosted yield to MMV positions, $LYRA emissions, and a multiplier for buying and selling rewards.

The method of unstaking is a bit completely different than what you is likely to be used to. You first must sign your intent to unstake, at which level a 14-day cooldown is initiated – throughout which the rewards are disabled. After this cooldown, a two-day window opens the place the staker wants to substantiate their motion with a view to unstake. If this window passes with out unstaking, their tokens will likely be staked once more and topic to a different 14-day cooldown ought to they attempt to unstake once more.

The Way forward for Lyra

Lyra not too long ago introduced their v2, consisting of an OP-stack primarily based rollup providing spot, perpetuals, and choices buying and selling. This appchain comes with a complete host of upgrades to Lyra, together with however not restricted to:

Portfolio margin, cross-margin, and multi-asset collateralCapital environment friendly spreads for optionsGas charges from the Lyra Chain accruing to Lyra DAOAn offchain matching engineAccount abstractionPartial liquidationsA model new UI

Learn extra about Lyra v2 right here. The early entry program can be accepting signal ups at present, you possibly can enroll right here. Lyra has executed over $500m of notional quantity up to now, making them the biggest onchain choices dex by a big margin. To place that into perspective within the bigger market – Deribit, the biggest centralized crypto choices alternate, clears 4 billion USD in quantity weekly. It’s clear decentralized choices nonetheless have an extended method to go, however with names like Lyra main the cost there’s clearly tons to be excited for.

{kind=link}